The most important facts in brief:

- Management participations are a key element of private equity very common.

- The aim of the participation is to create an incentive for the management to Increase enterprise value as much as possible.

- There is A lot of creative freedom in the structuring of the participation.

What is a management participation in private equity?

With a Management participation In a private equity fund, managing directors and senior executives of the portfolio company acquire a stake in a company. Private equity funds acquire companies in order to sell them again after approx. 5-10 years. During this time, the aim is to maximize the value of the company in order to achieve the greatest possible profit. In order for the management to create an incentive to increase the value of the company as much as possibleprivate equity funds invest the management in the companies.

- BackgroundManagement participation is therefore intended to avoid the so-called "principal-agent" problem and instead ensure that both the private equity fund and the management pursue aligned interests.

- ManagementManagement shareholdings are usually granted to the most important employees in the company. This typically includes the members of the management. Selected employees who are not part of the management are also given a partial stake in the company if they are expected to be able to exert a significant influence on the company's success.

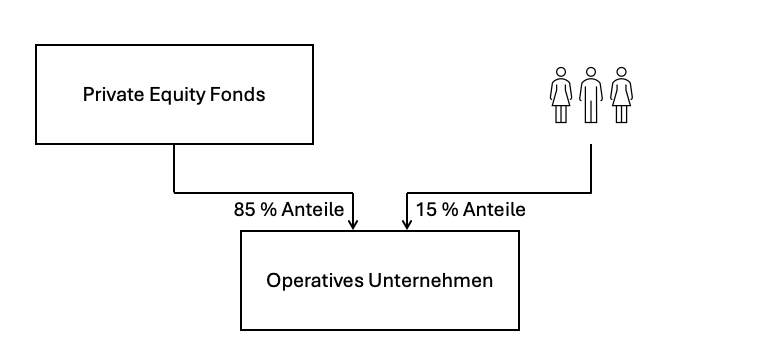

- ScopeIt is common for around 5-15 % of the shares in the company to be held by management.

What forms of management participation are there in private equity?

In abstract terms, there are two ways in which the management can participate in the company's performance: Either the management acquires part of the company itself or it concludes a contract with the private equity fund, under which the management does not participate in the company itself, but receives cash payments if predetermined targets are achieved.

There is a great deal of scope for structuring management participations. The following participation models are possible in private equity transactions:

- Direct participation

- Sweet Equity

- Sweat equity

- Virtual participation

What is direct participation?

In the case of a direct investment, the management acquires a direct stake in the company in the portfolio of the private equity fund. This form of management participation is rather rare in private equity. The background to this model is that the management has to pay the purchase price for the shares itself, which is associated with high costs. It is not possible to give the investment to the management as a gift, as the executives/managers involved would then have to pay taxes, but this would not be offset by any additional income. For this reason, direct management participation is very rare.

What is sweet equity?

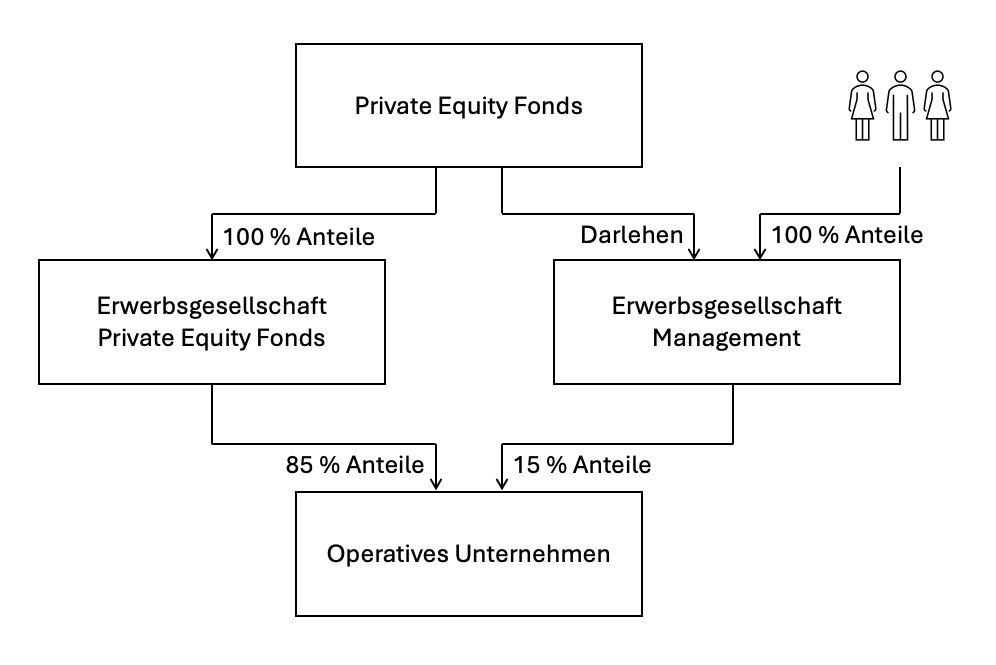

With sweet equity, the management acquires a stake in the company via an acquisition company (usually a GmbH or GmbH & Co. KG). In this case, the acquisition company must pay the purchase price for the shares in the company. The management assumes a portion of this (approx. 20 % of the purchase price). The private equity fund finances the remaining part of the purchase price via a loan to the management's acquisition company. The advantage of this approach is that the management only pays a pay a small part of the purchase price yourself must. Nevertheless, the management participates strongly in the performance of the company.

The management of the operating company should pay part of the purchase price itself so that the management also assumes its own risk (so-called "skin in the game") and is therefore particularly motivated.

Note: Sweat equity is the most popular form of employee participation among private equity funds.

What is sweat equity?

In the case of sweat equity, the management receives an option and thus the possibility of acquiring shares in the company at a later date at a fixed price. The difference to sweet equity is that the investment can only be acquired later, i.e. it still has to be earned (hence the term "sweat"). With the Option the exercise price is generally based on the current value of the shares. If the value of the company increases, the management will exercise the option because the exercise price does not increase and the shares can therefore be purchased very cheaply.

What is a virtual participation?

In the case of a virtual participation, the management will not acquire any shares in the company at a later date. At the same time, however, the management should still be incentivized and participate in the increase in value of the company. In the case of a virtual participation, the management therefore concludes an agreement with the private equity fund. contract, which usually places the management in the same position as in the case of Sweat Equity. The difference is that the management cannot acquire shares, but can receives the increase in value of the (virtual) company shares in cash.

The advantage of virtual participation is that it is very easy to implement, as only a contract needs to be concluded. The disadvantage, however, is that the subsequent payout must be taxed as wages in accordance with Section 19 of the German Income Tax Act (EStG), without the possibility of tax deferral via a holding company.

Tips for structuring management participation

Exactly how management participation is structured in private equity transactions depends on the circumstances of the individual case. There is no one solution that fits all situations. Rather Each design has its own advantages and disadvantages. When deciding on the form of participation and organization, you should consider the following aspects:

- Own riskIf the management invests its own money, this generally increases the connection with the company. By investing their own money, the management is threatened with a loss if the company does not perform well. At the same time, a financial investment can also be a deterrent and result in the remuneration package not being sufficiently attractive for competent management. A personal investment is only necessary in the case of direct participation or so-called "sweet equity". Such constructions are rather complex and lead in particular to an increase in the cost of replacing management. Accordingly, both sides should weigh up whether and to what extent the management should take on the risk itself.

- Leaver clausesIf the management is to be replaced or wishes to leave the company of its own free will, the shareholding in the company should also end. The background to this is that the management should benefit from the return on the work performed. If the management or individual managers no longer work for the company and therefore no longer contribute to its success, they should no longer participate in the company's success. Accordingly, all forms of management participation generally contain "leaver clauses" that regulate what happens to the participation in the event of termination. In principle, a distinction is made between ordinary termination by the manager and termination due to a serious breach of duty by the manager (so-called bad leaver events) and ordinary termination by the company or termination of the manager due to a breach of duty by the company (so-called good leaver events). In a Bad leaver case the manager often receives nothing or only the book value of his investment. In a good leaver case, the manager usually receives the market value of the investment upon termination. In the case of a direct participation or sweet equity, termination is much more complicated than in the case of options or virtual participations.

- Tax lawTax law: In the case of management participations, care must be taken to structure them in a tax-optimized manner and, in particular, to prevent so-called dry income from arising. In the case of dry income, the management receives income without any cash flow. This is disadvantageous for the management, as more taxes have to be paid without directly receiving more money with which to pay the taxes. In the case of genuine shareholdings, there is the possibility that the profit accrues in a holding company and therefore only has to be taxed at a low rate and is available for further investments without deductions.

- Co-disposal rights & obligationsThe aim of the investment is to encourage management to pursue the same objectives as the private equity fund. However, the management should often not be able to decide for itself whether, when and to whom it sells its shares, especially in view of a later sale of the operating company after 5 to 10 years. The management participation program should therefore contain co-sale rights and co-sale obligations (so-called drag-along and tag-along clauses).

- Dilution protectionIt is very important that the management protects itself against the dilution of its own investment. Otherwise, the private equity fund could significantly reduce the value of the investment unilaterally. At the same time, however, the private equity fund should be in a position to carry out a capital increase at a later date in order to invest additional money. The solution to this problem is often that the management receives subscription rights in the event of a capital increase. In the case of a virtual participation or options, corresponding compensation arrangements should be made.

- Revenue distributionIn the case of direct investments and sweet equity, arrangements are occasionally made to regulate the distribution of proceeds when the company is sold. The private equity fund receives its money first. Only when a predetermined return is achieved or exceeded does the management also receive part of the money.

- LoansPrivate equity funds occasionally grant loans to management so that they can use the money to acquire a stake. With such arrangements, it is important to ensure that the loans are made at normal market conditions in order to avoid gifts and the associated tax problems. At the same time, the loan should be structured in such a way that it does not overburden the management.